Market Sells Off as the Employment Cost Index (ECI) Report Aggravates Inflation Concerns

Market Sells Off as the Employment Cost Index (ECI) Report Aggravates Inflation Concerns

Follow me @TheBon_Scott on Twitter, and please share this newsletter if you find my work valuable.

The market received another dose of unwanted inflation data today. The Employment Cost Index (ECI), which measures employee compensation and benefits, increased 1.2% from December to March — the highest increase in a year — after rising 0.9% in the 4th quarter of 2023. The consensus expectation was for the ECI to rise 1.0%.

On balance, today's labor cost reading is not the end of the world for the Fed, but it is yet another data point that suggests the inflation slowdown stalled-out in the first quarter. This additional hot inflation number will further up the stakes for next month’s inflation readings after we’ve had 3 straight months of higher-than-expected inflation data.

The FOMC now has this additional data point to chew on before it makes its meeting announcement, tomorrow, and it’s another reason to be cautious in the near-term.

Treasury yields and the dollar rallied on the news, putting downward pressure on stocks — on top of already market nervousness going into tomorrow’s Fed meeting announcement.

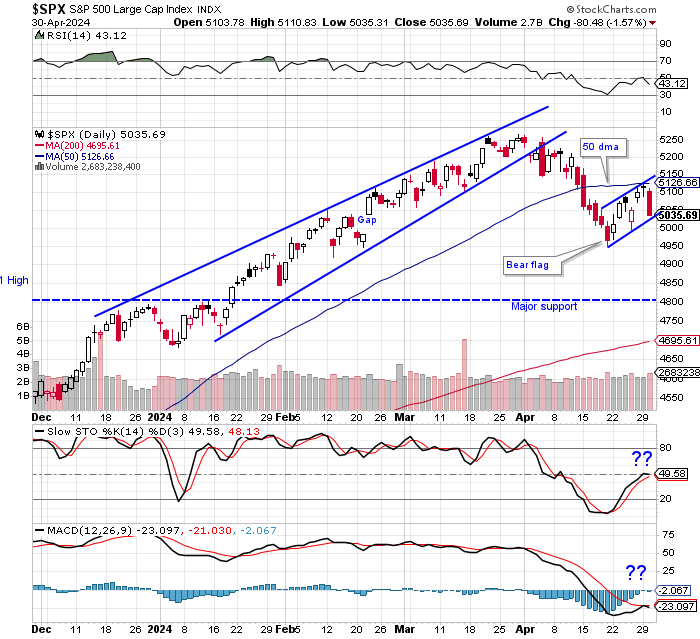

The S&P 500 dropped 1.57% on the day, and both the Nasdaq and small-cap Russell 2000 declined a bit over 2%. The S&P 500 has formed a bear flag, and traders should be on caution for a decisive breakdown through it on materially poor breadth. That would suggest a decline down to the 4800-4820 support area.

The Russell 2000 has also formed a bear flag, and the small-caps will be particularly sensitive/vulnerable to a further sizeable rally in Treasury yields.

Breadth was quite poor today, with declining stocks leading advancing stocks by nearly 5 to 1 on the NYSE, and 3 to1 on the Nasdaq. Bulls don’t want to see a repeat of this tomorrow.

I started a new short position today, currently my only one. And depending on any particularly “hawkish” tone in tomorrow’s Fed meeting statement and Powell’s post-meeting press conference — and the market’s reaction to it — I may very well add additional shorts. The market breadth and leadership, or lack thereof, will be the tell.

In earnings news, important AI names Super Micro Computer (SMCI), and Advanced Micro Devices (AMD), sold-off hard after-hours on their earnings reports/guidance, and that’s likely to spur some weakness in the semiconductor sector tomorrow. But mega-cap Amazon (AMZN), pleased the market with its earnings report as it reported robust cloud growth on growing AI demand. That should provide some downside cushioning in the tech and semi space.

The key of course, will be the Fed’s messaging at the conclusion of its meeting, and whether the market sees it as a glass that is half-full or half-empty. The Treasury market is going to drive the action, again. Another strong rise in yields will engender another broadly weak market day. Market bulls do not want to see the 10-year Treasury yield move over its April 25th high of 4.737%.

That’s is for now, I’ll write more soon. And as always, I’ll be posting frequent market commentary on WMI’s private Twitter (X) page.

Now, on to a new/updated long & short focus watchlist.

Focus Watchlist

I try to recommend trades that are timely and that a breakout/breakdown is likely to occur soon. If I take a stock or ETF off the focus watchlist, it may be because the trade needs more time to ripen, it ran away from us, or I’m no longer considering it at all.

Longs:

Keep reading with a 7-day free trial

Subscribe to Wade's Market Insights to keep reading this post and get 7 days of free access to the full post archives.